You’ll still apply with traditional financial institutions like banks and credit unions, since they administer the loans. And while FHA loans are federally insured, that protects the lender — not you — in case you default on the loan.

How much money do you need in the bank for a FHA loan?

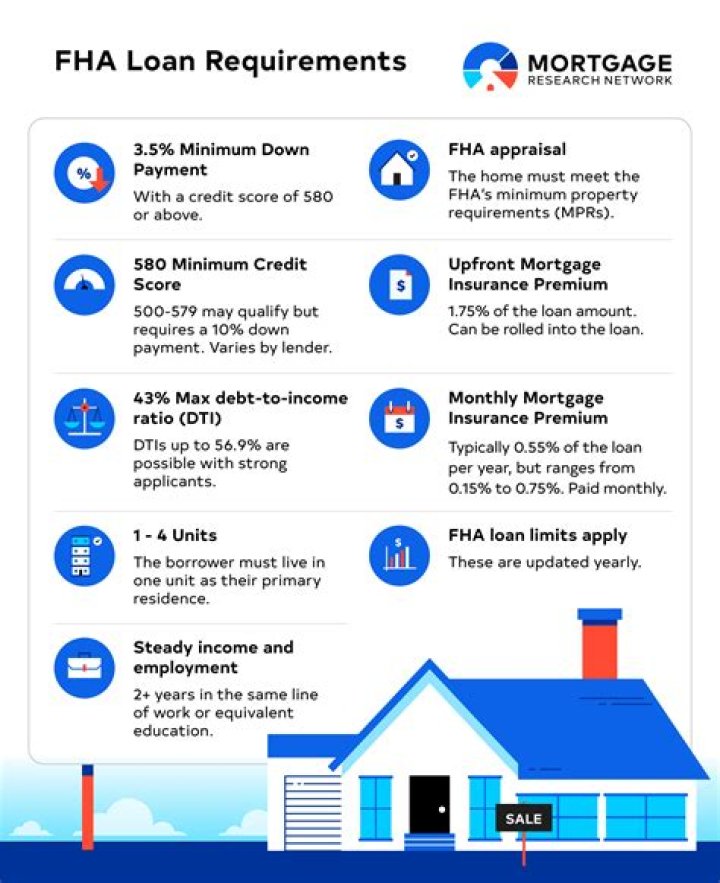

FHA loans have lower credit and down payment requirements for qualified homebuyers. For instance, the minimum required down payment for an FHA loan is only 3.5% of the purchase price.

How long does it take to get a FHA loan approved?

The entire FHA loan process takes between 30 days and 60 days, from application to closing.

What will disqualify you from an FHA loan?

According to the Department of Housing and Urban Development (HUD), you need a credit score of at least 500 to be eligible for an FHA loan. … If you fall well below this range, you might be denied for an FHA loan. In fact, bad credit is one of the most common causes of denial — for any type of mortgage loan.Does FHA help with down payment?

Down payment assistance may be available depending on what your state or local agencies might offer, but there is no down payment assistance program available from the FHA. … Both down payment assistance and contributions towards a borrower’s closing costs require strict verification and documentation by the lender.

Is a FHA loan worth it?

Advantages of FHA Loans Down payment: The 3.5% minimum down payment requirement on FHA loans is lower than what many (but not all) conventional loans require. If you have a credit score of about 650 or higher, the low down payment requirement is likely the main reason you’d be considering an FHA loan.

What percentage of FHA is denied?

Denials were higher — nearly 14 percent — for borrowers seeking government-backed loans (FHA, VA, USDA), and lower — 10.8 percent — for those applying for conventional mortgages eligible for purchase by investors Fannie Mae and Freddie Mac.

How do you know if you qualify for FHA loan?

- Have a FICO score of 500 to 579 with 10 percent down, or a FICO score of 580 or higher with 3.5 percent down.

- Have verifiable employment history for the last two years.

- Have verifiable income through pay stubs, federal tax returns and bank statements.

Do FHA loans take longer to close?

Industry data show that FHA loans do take longer to close than conventional, at least on average. … But the difference between their average closing times is typically just a matter of days.

Can you buy an as is home with an FHA loan?While HUD does not do their own loans, the Federal Housing Administration (FHA) does. “As-is properties may not qualify for government-insured loans like FHA or VA,” cautions Brook. “To qualify for this type of loan, properties cannot have defects like roof issues, chipping paint or other major deficiencies.”

Article first time published onHow much is closing cost?

Closing costs are typically about 3-5% of your loan amount and are usually paid at closing.

Why are FHA loans so difficult?

Unfortunately, some home sellers see the FHA loan as a riskier loan than a conventional loan because of its requirements. The loan’s more lenient financial requirements may create a negative perception of the borrower. And, on the other hand, the stringent appraisal requirements of the loan may make the seller nervous.

What does FHA look for in bank statements?

Required Documentation – The Mortgagee must obtain a gift letter signed and dated by the donor and Borrower that includes the following: -the donor’s name, address, and telephone number; – the donor’s relationship to the Borrower; – the dollar amount of the gift; and – a statement that no repayment is required.

Why is FHA bad?

FHA loans often come with higher interest rates than other loans, simply because they’re riskier. Since their credit score requirements are lower, there’s a bigger chance the borrower will default on the loan. To protect themselves from this added risk, lenders will charge a higher interest rate.

Is Conventional better than FHA?

FHA loans allow lower credit scores than conventional mortgages do, and are easier to qualify for. Conventional loans allow slightly lower down payments. … FHA loans are insured by the Federal Housing Administration, and conventional mortgages aren’t insured by a federal agency.

What is the minimum down payment for a house?

The minimum down payment required for a conventional loan is 3%. And the minimum down payment for an FHA loan is 3.5%. Some special loan programs even allow for 0% down payments. But still, a 20% down payment is considered ideal when purchasing a home.

Do lenders check bank statements before closing?

Do lenders look at bank statements before closing? Lenders typically will not re–check your bank statements right before closing. They’re only required when you initially apply and go through underwriting.

What credit score do FHA lenders use?

FHA Loan Down Payments Your credit score is a number ranging from 300 to 850 that’s used to indicate your creditworthiness. An FHA loan requires a minimum 3.5% down payment for credit scores of 580 and higher. If you can make a 10% down payment, your credit score can be in the 500 – 579 range.

Where can I apply for a FHA loan?

Where can I apply for an FHA loan? The FHA doesn’t offer loans directly, so you’ll need to contact a private lender to apply. The majority of lenders are FHA–approved, so you’re free to choose a local lender, big bank, online mortgage lender, or credit union.

What is the minimum credit score for a conventional loan?

Conventional Loans A conventional loan is a mortgage that’s not insured by a government agency. Most conventional loans are backed by mortgage companies Fannie Mae and Freddie Mac. Fannie Mae says that conventional loans typically require a minimum credit score of 620.

What credit score does a first time home buyer need?

FICO® Scores☉ of at least 640 or so are typically all that are needed to qualify for first-time homebuyer assistance. FICO® Scores range from 300 to 850. But chances are you may need higher credit scores of around 680 or so to qualify for a conventional mortgage.

How can I avoid closing costs?

- Look for a loyalty program. Some banks offer help with their closing costs for buyers if they use the bank to finance their purchase. …

- Close at the end the month. …

- Get the seller to pay. …

- Wrap the closing costs into the loan. …

- Join the army. …

- Join a union. …

- Apply for an FHA loan.

Can you negotiate closing costs?

The short answer is yes – when you’re buying a home, you may be able to negotiate closing costs with the seller and have them cover a portion of these fees.

How long does it take to close on a house?

You can expect closing on a house to take 30 – 50 days, though closing day itself typically takes no longer than a few hours. But closing on a house is a multistep process, which takes time. So, your experience may differ depending on the type of loan you choose and potential delays, such as repairs.

Why do Realtors hate FHA loans?

With FHA loans, their hands are tied – they either lower the price or list the home again. … The other major reason sellers don’t like FHA loans is that the guidelines require appraisers to look for certain defects that could pose habitability concerns or health, safety, or security risks.

What are the FHA loan limits for 2020?

Thanks to increases in home prices in 2019, the Federal Housing Administration loan limit will increase for nearly all of the country in 2020. According to an announcement from the FHA, the 2020 FHA loan limit for most of the country will be $331,760, an increase of nearly $17,000 over 2019’s loan limit of $314,827.

How far back do banks check for mortgage?

How far back do mortgage credit checks go? Mortgage lenders will typically assess the last six years of the applicant’s credit history for any issues.

How do I qualify for a bank loan?

- Must provide 12 months of consecutive bank statements from the same account.

- 20% down payment required, or 10% with mortgage insurance.

- 45% maximum debt-to-income ratio.

- $1,000,000 maximum loan amount, $200,000 minimum.

- Must escrow for taxes and insurance.

How long does it take to get a mortgage approved?

Generally speaking, it usually takes two to six weeks to get a mortgage approved. The application process can be accelerated by going through a mortgage broker who can find you the best deals that suit your circumstances. A mortgage offer is usually valid for 6 months.

Can I sell my FHA home?

The short answer is yes, in most cases it’s entirely possible to sell a home even if you’re still paying on FHA loan. There is no rule or requirement that says you cannot sell a house while you still have an FHA loan associated with the property.

Does seller have to pay FHA closing costs?

FHA loans allow sellers to cover closing costs up to six percent of your purchase price. That can mean lender fees, property taxes, homeowners insurance, escrow fees, and title insurance. Naturally, this kind of help from sellers is not really free.