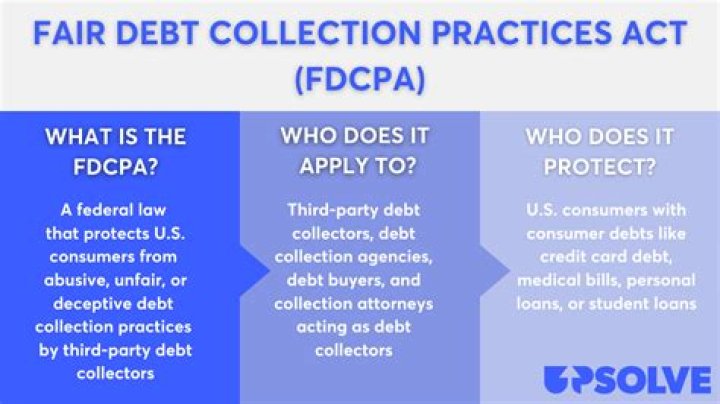

The FTC enforces the Fair Debt Collection Practices Act (FDCPA), which makes it illegal for debt collectors to use abusive, unfair, or deceptive practices when they collect debts.

What is the most common violation of the FDCPA?

- Continued attempts to collect debt not owed. …

- Illegal or unethical communication tactics. …

- Disclosure verification of debt. …

- Taking or threatening illegal action. …

- False statements or false representation. …

- Improper contact or sharing of info. …

- Excessive phone calls.

What are four practices that collectors are prohibited from doing under the FDCPA?

Along with other restrictions, they cannot: Solicit postdated checks for payment to use as a threat or for the purposes of instituting criminal prosecution. Deposit or threaten to deposit a postdated check before your intended payment date. Take or threaten to take property if it’s not allowed.

What is considered a violation of FDCPA?

Deceptive practices include making false representations about the amount or legal status of your debt, making false threats to take legal action, or otherwise deceiving you to get you to pay. … Engaging in any practice that forces you to pay additional money other than the debt you owe is considered an FDCPA violation.What are the penalties for violating the FDCPA?

Common Violations of the Fair Debt Collection Laws Creditors, professional debt collectors, and attorneys who violate the law are subject to paying actual damages, statutory penalties of $1,000 and the consumer’s attorneys fees and costs.

Can you go to jail for being in debt?

You cannot be arrested or go to jail simply for being past-due on credit card debt or student loan debt, for instance. If you’ve failed to pay taxes or child support, however, you may have reason to be concerned.

Can you sue a creditor for violating the FDCPA?

File a Lawsuit Against the Debt Collector If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.

Can I sue a debt collector for emotional distress?

You have the right to sue a debt collector, creditor, or agency if they are harassing you. This kind of behavior from a debt collector can cause emotional hardship such as stress and anxiety. These things impact the consumer, as well as close family and friends.Who qualifies for protection under FDCPA?

It also protects reputable debt collectors from unfair competition and encourages consistent state action to protect consumers from abuses in debt collection. The FDCPA applies only to the collection of debt incurred by a consumer primarily for personal, family, or household purposes.

Can I be chased for debt after 10 years?In most cases, the statute of limitations for a debt will have passed after 10 years. This means a debt collector may still attempt to pursue it (and you technically do still owe it), but they can’t typically take legal action against you.

Article first time published onWho is covered by the FDCPA?

The FDCPA only applies to third-party debt collectors, such as those who work for a debt collection agency. Credit card debt, medical bills, student loans, mortgages, and other kinds of household debt are covered by the law.

Which type of debt is not covered by the FDCPA?

Debts that may not be covered are those that are not incurred voluntarily, such as income taxes, parking and speeding tickets, and domestic support obligations like child support and alimony, or spousal support.

Does FDCPA apply to medical bills?

Federal Debt Collection Practices Act, 15 U.S.C. 1692 et seq. Only consumer debts – acquired primarily for personal, family or household purposes – are covered by the FDCPA. Therefore, medical debt, which is acquired for a personal purpose, is subject to the Act.

What factors are considered by a court when determining the size of damage awards for Fdcpa violations?

In determining the amount of statutory damages to be awarded in a particular case, a court shall consider, among other factors, “the frequency and persistence of noncompliance by the debt collector, the nature of such noncompliance, and the extent to which such noncompliance was intentional.” 15 U.S.C.

What is a validation notice?

Collectors are required by Fair Debt Collection Practices Act to send you a written debt validation notice with information about the debt they’re trying to collect. It must be sent within five days of the first contact. The debt validation letter includes: The amount owed. The name of the creditor seeking payment.

What debt collectors Cannot do?

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

Is not paying a loan a crime?

The Consumer Financial Protection Bureau, which is responsible for regulating payday lending at the federal level is very clear: “No, you cannot be arrested for defaulting on a payday loan.” A U.S. court can only order jail time for criminal offenses, and failure to repay a debt is a civil offense.

Can you be stopped at airport for debt?

NO, you can’t get stopped at the airport for debt, and you can’t get arrested for debt. Talking legally, a debt collector can’t even say they will arrest you. Legally you can’t get stopped at the airport just because you owe money in some ways.

What happens if a Judgement is not paid?

If you do not pay the judgment, the judgment creditor can garnish or “seize” your property. The judgment creditor can get an order that tells the Sheriff to take your personal property, like the money in your bank account or your car, to pay the judgment.

Can an individual debt collector be sued under the Fdcpa?

If a collector has violated the FDCPA, you can sue that collector in court. You might be able to recover the following types of damages, including monetary damages, attorneys’ fees, and more.

How do I sue a creditor for harassment?

If you believe a debt collector is harassing you, you can submit a complaint with the CFPB online or by calling (855) 411-CFPB (2372). You can also contact your state’s attorney general .

Is it true that after 7 years your credit is clear?

Even though debts still exist after seven years, having them fall off your credit report can be beneficial to your credit score. … Note that only negative information disappears from your credit report after seven years. Open positive accounts will stay on your credit report indefinitely.

Is a debt written off after 6 years?

For most debts, if you’re liable your creditor has to take action against you within a certain time limit. … For most debts, the time limit is 6 years since you last wrote to them or made a payment. The time limit is longer for mortgage debts.

How long can a credit card company come after you?

A statute of limitations is a law that tells you how long someone has to sue you. In California, most credit card companies and their debt collectors have only four years to do so. Once that period elapses, the credit card company or collector loses its right to file a lawsuit against you.

Are servicers debt collectors?

In most cases, the defaulted borrower will allege that because the loan was in default at the time the mortgage servicer began servicing the loan (after an assignment), the servicer is a “debt collector.” That alone does not qualify the servicer as a debt collector.

What is a FDCPA letter?

What Is an FDCPA Validation Letter? The FDCPA is a federal law that protects consumers from abusive collection practices by debt collectors and collection agencies. Whether the FDCPA applies to foreclosures generally depends on if the foreclosure is judicial or nonjudicial. Judicial foreclosures.

Can I pay the original creditor instead of the collection agency?

Even if a debt has passed into collections, you may still be able to pay your original creditor instead of the agency. … The creditor can reclaim the debt from the collector and you can work with them directly. However, there’s no law requiring the original creditor to accept your proposal.

Can debt collectors call your family?

The short answer is, yes, debt collectors can call third parties like relatives or friends. But the law limits what they can say. They’re really only supposed to call third parties if they can’t reach you or don’t have your contact information.

What is the minimum amount that a collection agency will sue for?

The minimum amount a collection agency will sue you for is usually $1000. In many cases, it is less than this. It will depend on how much you owe and if they have a written contract with the original creditor to collect payments from you.

What should you not say to debt collectors?

- Never Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. …

- Never Admit That The Debt Is Yours. Even if the debt is yours, don’t admit that to the debt collector. …

- Never Provide Bank Account Information.